DPC to Congress: Patients Deserve Care—Not Insurance Red Tape

In light of hearings on the cost of healthcare being held by the U.S. House Energy & Commerce Health Subcommittee today, the Domestic Policy Caucus is calling on Congress to focus on red tape and bureaucracy that hinders patients from getting the healthcare they need…

In light of hearings on the cost of healthcare being held by the U.S. House Energy & Commerce Health Subcommittee today, the Domestic Policy Caucus is calling on Congress to focus on red tape and bureaucracy that hinders patients from getting the healthcare they need.

Health insurance is supposed to provide peace of mind when illness strikes. Yet for far too many Americans, coverage comes with a maze of administrative obstacles that delay treatment, increase costs, and leave patients wondering whether they will receive the care their physicians recommend.

Most Americans believe insurer prior authorization requirements are a burden, and many say insurance red tape is the biggest challenge they face when they are sick and navigating the healthcare system. These hurdles often require physicians to obtain insurer approval before patients can receive medications, procedures, or other medically necessary services—even when those services are ultimately approved.

This system creates unnecessary delays for patients while diverting physicians and healthcare staff away from patient care and toward paperwork. If insurers routinely approve a particular treatment more than 90 percent of the time, policymakers should ask why that service remains subject to prior authorization in the first place. Streamlining or eliminating these requirements for consistently approved services would reduce waste, lower administrative costs, and help patients receive timely care.

Greater insurer accountability is essential. Health plans should be transparent about denial rates, approval timelines, and the clinical evidence supporting their coverage decisions. Patients deserve clear explanations when care is delayed or denied, and providers should not be forced to spend countless hours appealing decisions that ultimately prove medically appropriate.

Healthcare affordability is about more than premiums and deductibles. Administrative barriers imposed by insurers carry real costs—in delayed diagnoses, postponed treatments, higher provider overhead, and unnecessary frustration for patients and families.

A healthcare system that works for patients must hold every stakeholder accountable. That includes insurers. Reducing unnecessary administrative barriers, improving transparency, and ensuring timely access to medically necessary care are practical reforms that would strengthen the healthcare system while putting patients—not paperwork—at the center of healthcare.

That’s why the Domestic Policy Caucus is pleased to see the U.S. House Energy & Commerce Health Subcommittee turn its attention toward healthcare costs. We hope the focus lands where it belongs.

Read more in this insightful column by Sally Pipes of the Pacific Research Institute

DPC in The Detroit News: Small-dollar loans aren't predatory -- they're a lifeline

The Domestic Policy Caucus penned an op-ed, "Small-dollar loans aren't predatory -- they're a lifeline," for The Detroit News…

The Domestic Policy Caucus penned an op-ed, "Small-dollar loans aren't predatory -- they're a lifeline," for The Detroit News.

In part, DPC wrote, "The benefits of small-dollar loans from non-bank institutions are often overlooked by people who have no personal experience with them."

Read the full op-ed here.

DPC Applauds Court Ruling Against North Dakota Legislature’s Attempted 340B Abuse

The Domestic Policy Caucus applauds an April 27 ruling by U.S. District Court Judge Daniel M. Traynor that quashes the North Dakota Legislature’s attempt, through the recently passed House Bill 1473, to “facilitate and sanction the graft” associated with abuse of the 340B drug pricing program…

The Domestic Policy Caucus applauds an April 27 ruling by U.S. District Court Judge Daniel M. Traynor that quashes the North Dakota Legislature’s attempt, through the recently passed House Bill 1473, to “facilitate and sanction the graft” associated with abuse of the 340B drug pricing program.

The 340B program, established in 1992, compels prescription drug manufacturers to provide deeply discounted drugs to certain clinics and hospitals, with the understanding that the clinics and hospitals will either pass along the saving to patients, or charge insurers the full price and then use the profits to provide additional charity care. Participating in the 340B program is required for manufacturers who want to participate in federal Medicaid and Medicare programs.

With no restrictions on how 340B funds are used and few reporting requirements, many hospital systems are abusing the program and using it to amass huge profits at the expense of patients, employers, unions, and taxpayers.

In a sharply worded summary judgment in favor of AbbVie Inc. and Pharmaceutical Research and Manufacturers of America (PhRMA), Judge Traynor agreed with pharmaceutical companies that while the law purports to “protect the underdogs,” it illegally interferes with the federal drug-pricing regime.

Judge Traynor said, “The states defending these laws say those populations [poor, underinsured, vulnerable] are the ones hurt when pharmaceutical companies put certain restrictions on delivery under the 340B program… However, a program meant to help American poor is being abused to provide a windfall to hospital conglomerates and participating pharmacies… North Dakota’s law attempts to facilitate and sanction the graft by interfering with an area of federal law… Here is what is really going on: a coordinated collusion between the state’s covered entities and contract pharmacies to exploit Congress’ inattention to a federal program. As a result, pharmacies and third-party administrators pocket billions of dollars each year… Manufacturers should [not] be fleeced by enterprising states and hospital conglomerates that wield power in legislative lobbies… Ultimately, it’s the patients who suffer… The 340B drug pricing program was meant to help the needy who require medication to live. H.B. 1473 benefits hospital conglomerates and Joe Paycheck sees no difference in the price of his meds… H.B. 1473 is an infringement on federal programs masquerading as state governance.”

Read the full LAW360 article about the decision here.

The court ruling represents an excellent example of the checks and balances that our nation’s founders envisioned. In this case, a federal judge has quashed overreach by the rogue North Dakota legislature, to the benefit of American patients, employers, unions, and taxpayers.

The Domestic Policy Caucus applauds Judge Traynor’s judgment.

National Popular Vote Appears in the Washington Examiner

National Popular Vote senior consultant, Patrick Rosenstiel, recently penned an op-ed in the Washington Examiner imploring conservatives to embrace the National Popular Vote, while disproving some common misconceptions about the Compact.

National Popular Vote senior consultant, Patrick Rosenstiel, recently penned an op-ed in the Washington Examiner imploring conservatives to embrace the National Popular Vote, while disproving some common misconceptions about the Compact.

In the article, Rosenstiel said, in part, “The conservative movement should embrace reform that makes every voter in every state politically relevant in every presidential election. I believe that our ideas are better, more aligned with most voters, and can win presidential elections. President Donald Trump bolstered this belief when he won the national popular vote in 2024.”

Read the full op-ed here.

DPC in Duluth (Minn.) News Tribune: Minnesota, Wisconsin consumers deserve more, not fewer, credit options

From the column: “Americans with modest means deserve the same range of financial tools as those who are better off.”…

From the column: “Americans with modest means deserve the same range of financial tools as those who are better off… Any credit-restriction proposal that comes up in Minnesota or Wisconsin should be given no consideration.”

Read the full column here.

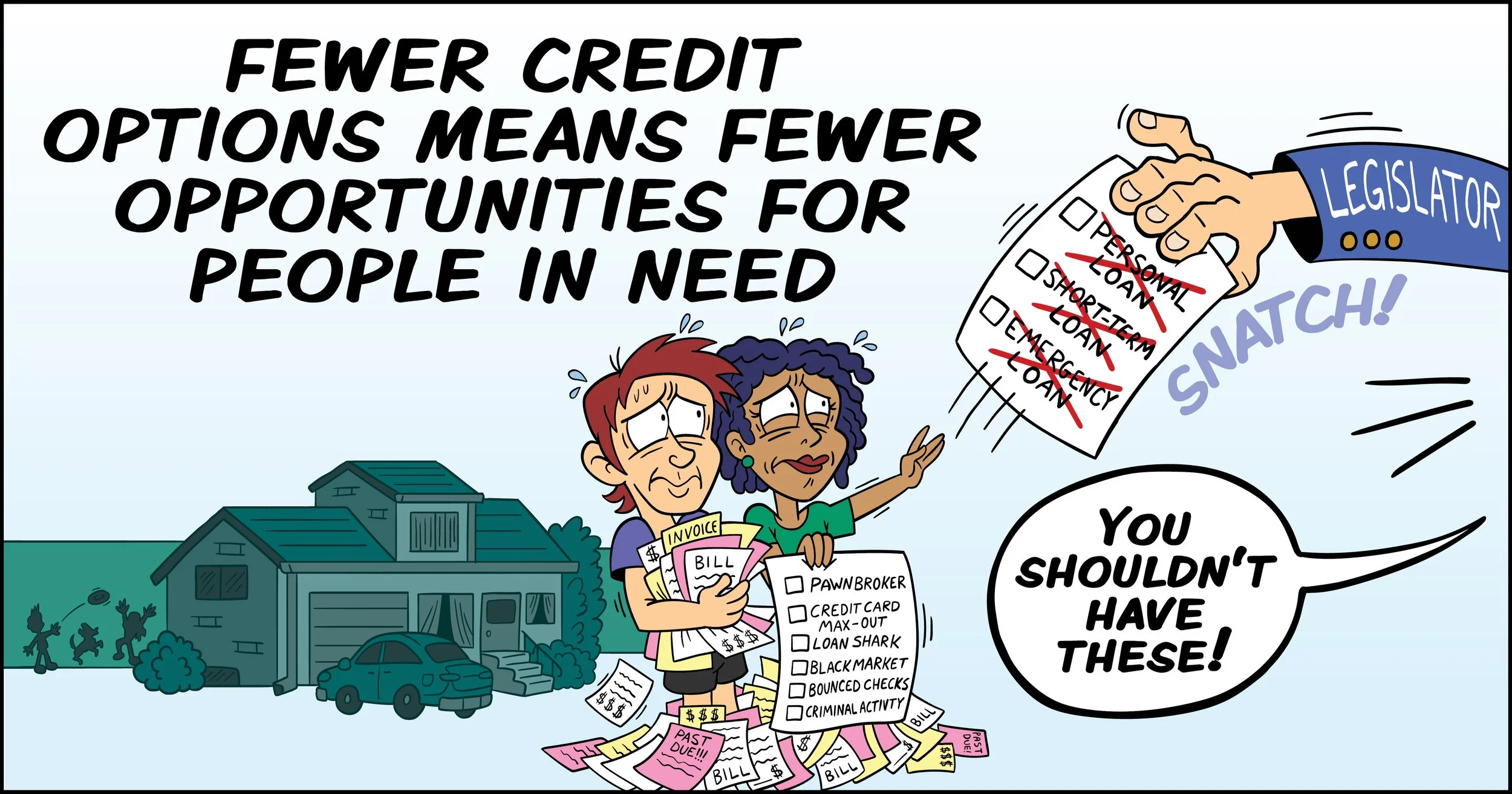

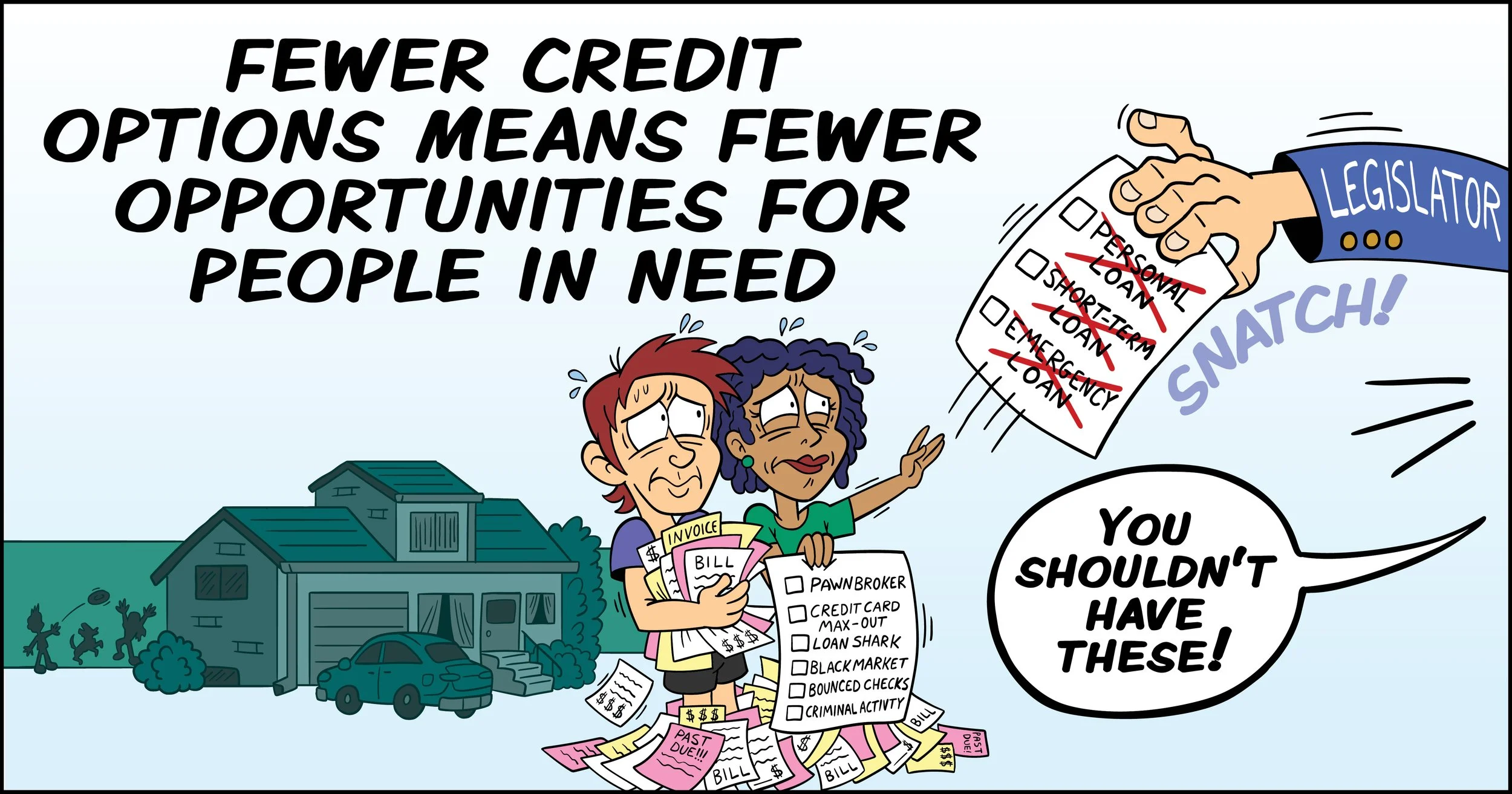

DPC Offers “Freedom to Borrow” Editorial Cartoon

Imposing interest rate caps on loans and restricting the credit options available to consumers are ill-conceived policies that do not achieve their desired outcome. The Domestic Policy Caucus is working to educate policymakers and stakeholders about this fact…

Imposing interest rate caps on loans and restricting the credit options available to consumers are ill-conceived policies that do not achieve their desired outcome. The Domestic Policy Caucus is working to educate policymakers and stakeholders about this fact.

Such policies unfairly target short-term, small-dollar loans that many disenfranchised and disadvantaged people use. People with subprime credit scores or “underbanked” or “unbanked” people often rely on these types of loans and other creative financing solutions to access credit for car repairs, to pay rent, or in a medical emergency.

Credit rate caps reduce purchasing power, not by making credit cheaper for everyone, but by limiting access to credit for many consumers, especially those with lower incomes or credit scores who need it most.

Without credit options, borrowers may turn to more damaging alternatives: overdrawing accounts, accumulating credit card debt they cannot repay, declaring bankruptcy, or seeking out unregulated, black-market lenders with far harsher terms.

Americans with modest means deserve the same range of financial tools as those who are better off. Preserving access to a variety of credit options is essential—not only to help families weather short-term challenges but also to give them a pathway toward greater financial stability and opportunity.

To drive home these points, the Domestic Policy Caucus has produced this editorial cartoon and encourages anyone and everyone to download and use it with newspaper columns, blogs, social media posts, and so on.

DPC Discusses Freedom to Borrow on The Jack Tomczak Show on WWTC Radio

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., substitute-hosted the Jack Tomczak Show on WWTC AM1280 The Patriot radio in the Twin Cities, with guest Patrick Brenner, President and CEO of the Southwest Public Policy Institute…

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., substitute-hosted the Jack Tomczak Show on WWTC AM1280 The Patriot radio in the Twin Cities, with guest Patrick Brenner, President and CEO of the Southwest Public Policy Institute.

Kaiser and Brenner discussed efforts to restrict access to credit and impinge on the freedom to borrow.

Listen below.

DPC Provides Testimony in Opposition to Minnesota House File 3609

The Domestic Policy Caucus provided written testimony in opposition to Minnesota House File 3609, which would cement the current, flawed 340B policy in the state, for the March 18, 2026, meeting of the House Health Finance & Policy Committee…

The Domestic Policy Caucus provided written testimony in opposition to Minnesota House File 3609, which would cement the current, flawed 340B policy in the state, for the March 18, 2026, meeting of the House Health Finance & Policy Committee.

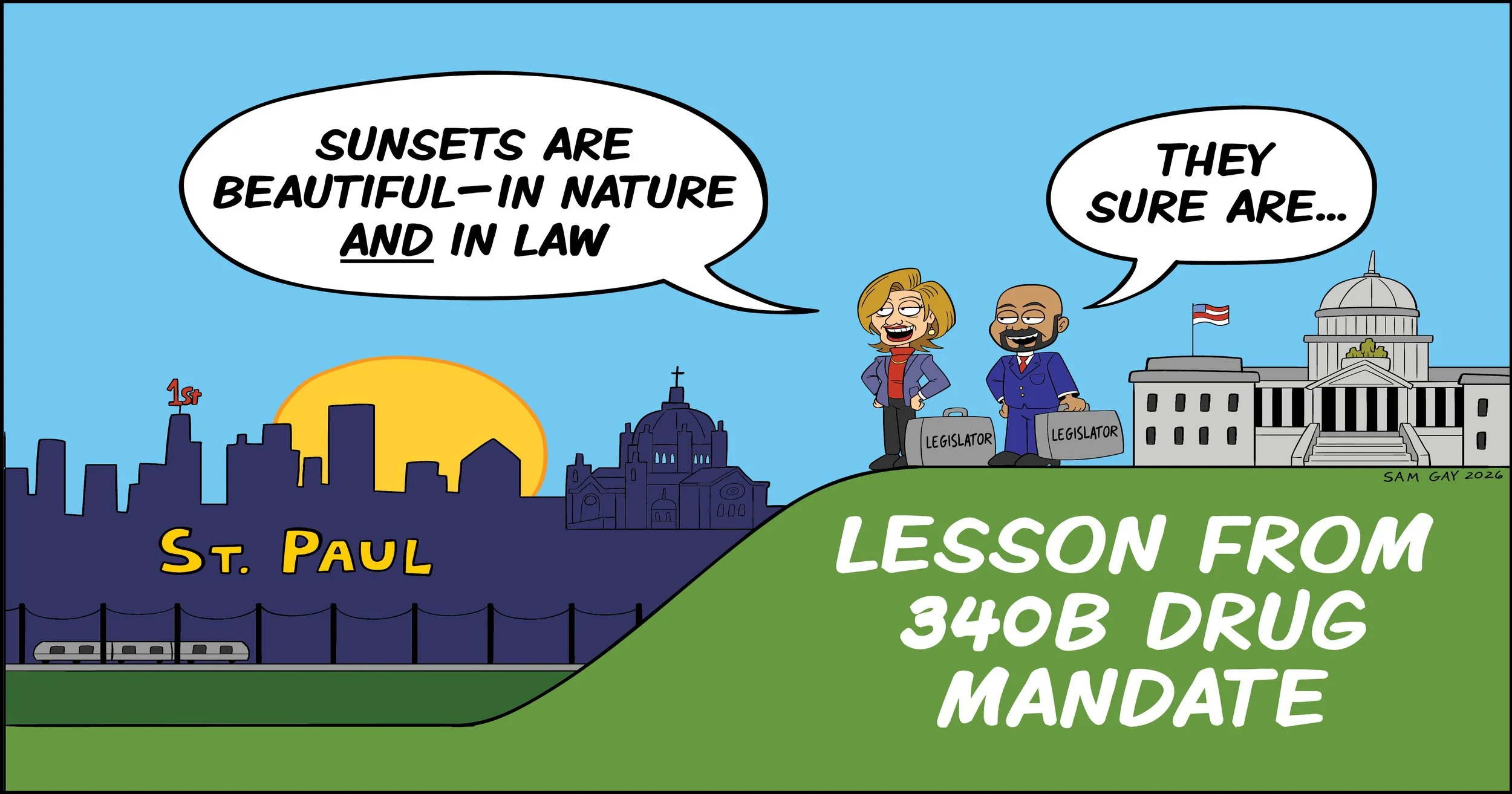

In part, DPC wrote, “Current 340B legislation has a sunset clause extending to the middle of 2027. There is no need to act on 340B in Minnesota before next year… Proposing H.F. 3609 at this time is premature… At a time when Minnesota is mired in a regime of fraud and abuse, it is not appropriate to push forward with another massive program that lacks transparency and reeks of abuse. If you move forward with H.F. 3609, then you are voting to be part of the problem… The sunset provision in the current law is an opportunity. Just like sunsets in nature give you the opportunity to reflect on the day and look forward to a better day tomorrow, a sunset provision like the one in the current law regarding 340B gives you the opportunity to look reflect on how the law has worked and where it needs reform and to make changes before the sunset comes in the summer of 2027 so that 340B serves Minnesotans in the best way possible.”

Read the complete testimony here.

DPC Provides Testimony in Opposition to Minnesota Senate File 3769

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., provided testimony at the March 3, 2026, meeting of the Minnesota Senate Commerce and Consumer Protection Committee…

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., provided testimony at the March 3, 2026, meeting of the Minnesota Senate Commerce and Consumer Protection Committee.

In part, DPC testified, "The current 340B law has a sunset clause extending to the middle of 2027. So, there is no need to act on 340B in Minnesota before next session. The sunset provision provides an opportunity to study the 340B track record in Minnesota and get it right going forward—not to rush into cementing a flawed program into place... Please oppose S.F. 3769 and use this year and a half before the current law sunsets to get 340B right in Minnesota."

Read the full testimony here.

DPC Provides Further Testimony on Oregon House Bill 4116, DIDMCA Opt-Out

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., provided further testimony on Oregon House Bill 4116—this, before the Senate Committee on Labor and Business, on February 23, having testified earlier this month before the House Commerce and Consumer Protection Committee…

Domestic Policy Caucus Secretary/Treasurer Kent Kaiser, Ph.D., provided further testimony on Oregon House Bill 4116—this, before the Senate Committee on Labor and Business, on February 23, having testified earlier this month before the House Commerce and Consumer Protection Committee.

DPC testified:

According to the Oregon State Treasury:

Nearly 17% of Oregonians have non-prime credit scores.

About 37% of Oregonians say they couldn’t cover a $400 emergency expense.

These are among the consumers who would be harmed by House Bill 4116, and you’d be pushing them into situations where they might gravitate toward desperate, maybe black market, options such as loan sharks. And many will choose black market options because they don’t have items to sell, which is one option that the bill’s proponents have often suggested. Others will choose the black market over the awkwardness of asking a family member or friend for short-term emergency loans, which is the other option that proponents of the bill have naively suggested.

If you are inclined to support this bill, please think about this: How many items do you personally own that you could sell for $400 quickly in an emergency? What about when a second or third emergency comes up? What would you sell then? Now, set aside your privilege and think about someone who is far less well off than you are—someone who doesn’t have much stuff to sell or much stuff that’s even worth $400 or acquaintances with enough money to buy the stuff. The prospect of coming up with $400 for an emergency expense is pretty bleak.

Now, if you are inclined to support his bill, please think about a 24-year-old coming up a little short on the monthly rent. He might turn to his mother today and say, “Hey, ma, could you loan me $100 to cover the rent? I can pay ya back on Friday.” And she says, “Sure, son, but you have to pay me a dollar a day for the loan.” Of course, the kid will take the deal—it’s a great deal. Indeed, this is the ideal scenario according to proponents of House Bill 4116. It’s also a 365% APR in an unregulated context that doesn’t help the kid build his credit score. And remember, many of the people in a similar situation come from families where no one has $100 to loan to a needy kid.

You wouldn’t send someone to the Alvord Desert without a water bottle. You shouldn’t banish poor Oregonians to a veritable credit desert with no way to purchase what they need to survive, either.

Please oppose House Bill 4116.